Real estate markets, financial stability and macroprudential policy

Credit-fuelled real estate booms can pose financial stability risks due to the important direct and indirect links between real estate markets, the economy and the financial system. Different types of macroprudential policy tools can be used to increase resilience to financial stability risks from residential real estate (RRE) markets. Borrower-based tools put a cap on the risk characteristics of new loans, while capital-based tools increase the loss absorption capacity of banks. The ECB, together with the national authorities, has an important role to play in shaping the macroprudential policy response to RRE risks in the euro area.

1 The importance of real estate markets for financial stability

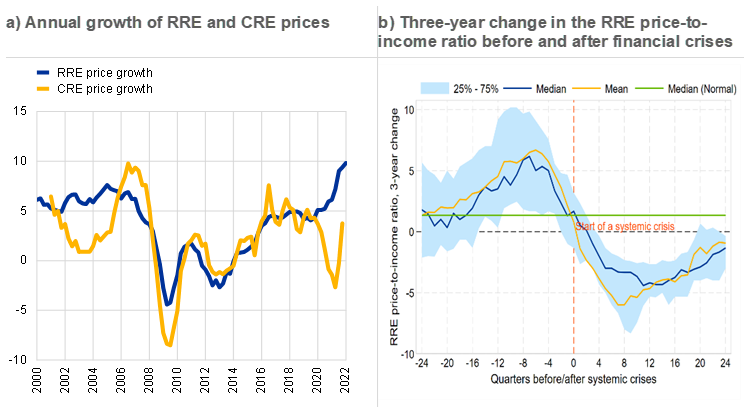

Developments in real estate markets have received heightened attention in recent years. As highlighted in the ECB’s May 2022 issue of the Financial Stability Review, euro area nominal RRE price growth has accelerated sharply since 2020 to reach the highest growth rate of the last 20 years (Chart 1, panel a) amid robust annual mortgage lending growth. These developments have led to concerns about increasing RRE price overvaluation and household indebtedness.[1] At the same time, commercial real estate (CRE) markets seem to be stabilising after a sizeable price correction during the COVID-19 pandemic (Chart 1, panel a), but conditions remain challenging in some market segments. This lead article of the Macroprudential Bulletin discusses why developments in real estate markets are important for financial stability and what macroprudential policy can do to mitigate the risks.

Real estate markets are important from a macroeconomic and financial stability perspective, as shown by past crises. The 2008 global financial crisis (GFC) is the most prominent example of the potentially large negative effects of real estate boom-bust cycles for the economy and the financial system. In the run up to the GFC real estate prices increased substantially accompanied by sustained increases in credit provision, and prices collapsed once the financial crisis started and the imbalances began to unravel. This real estate boom-bust pattern is common ahead of financial crises (Chart 1, panel b). Indeed, recent research has shown that credit-fuelled real estate bubbles significantly increase the risk of a financial crisis, and that when such bubbles collapse, they are associated with deeper and longer recessions.[2] The fact that past financial crises in European countries have led to average output losses of 8%[3] shows that credit-fuelled real estate bubbles can indeed be very costly for the society.

Chart 1

Developments in real estate markets have received heightened attention in recent years, given that real estate booms have often preceded financial crises in the past

Sources: ECB.

Notes: Panel b) The blue shaded area indicates the interquartile range of the indicator across euro area countries plus Denmark, Sweden and the UK during the quarters before and after systemic financial crises. The green line indicates the median of the indicator across the same set of countries in “normal times” (not within +/- six years of the start of a systemic financial crisis). The dating of systemic financial crises in the chart is based on the ECB/European Systemic Risk Board (ESRB) crises database referred to in Lo Duca, M. et al. (2017). Purely foreign-induced crises are excluded.

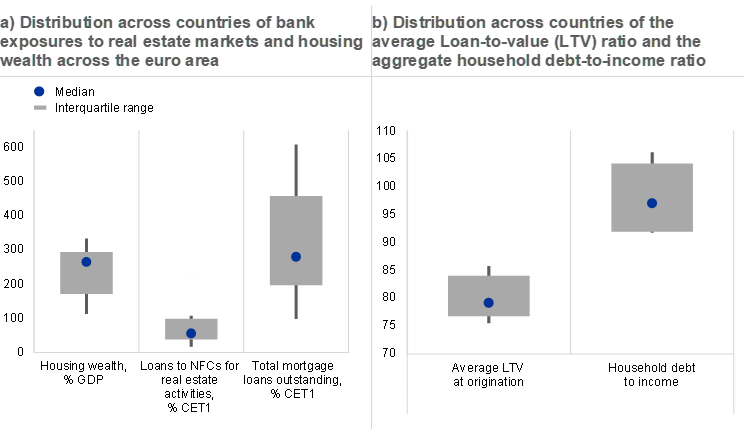

The systemic importance of real estate markets stems from the strong link between them and significant parts of the economy. First, real estate-related investment (construction), consumption and services make up a significant share of the economy. Second, the financial sector, and in particular banks, have a primary role in financing real estate investments. Bank mortgage loan portfolios exceed 200% of banks’ CET1 capital in most euro area countries, and loans to companies engaging in real estate activities are also of significance in several of them (Chart 2, panel a). Finally, real estate properties are a very important form of storage of wealth for households, worth more than 200% of GDP in most euro area countries (Chart 2, panel a).

Ultimately, high leverage and strong links with the economy shape the transmission of real estate boom-bust cycles to the financial system. Real estate purchases are often financed with a high share of debt (Chart 2, panel b), and high leverage in turn means high sensitivity of expenditure and potential defaults to corrections in real estate markets. First, if leverage is high, even small declines in real estate prices lead to a significant decline in household wealth and in the net worth of firms who own a property; this, in turn, tends to reduce their willingness and ability to borrow, consume and invest[4]. Lower expenditure and investment may then cause economic activity to contract and lead to a recession. Second, high household and corporate indebtedness imply lower financial buffers and less resilience in situations where income or real estate prices decline, which increases the likelihood of widespread loan defaults. Given that banks and the wider financial system tend to be heavily exposed to the real estate sector, higher real estate-related loan defaults could, in turn, cause distress for banks and for the wider financial system.

Chart 2

There are strong links between real estate markets, the economy, and the financial system, including bank exposures to real estate and household property ownership

Sources: Panel a: ECB; panel b: ECB and European DataWarehouse (EDW).

Notes: The lower and upper hinges correspond to the 25th and 75th percentiles. The upper whisker extends from the hinge to the largest value, no further than 1.5 * Interquartile Range (IQR) from the hinge. Extreme values are not shown. In panel a, the latest observations are for quarter 1, 2022. NFCs stands for non-financial corporations. In panel b, the average LTV per country is based on a weighted average by origination balance for loans originated in 2020. EDW data cover the following euro area countries: BE, DE, IE, ES, FR, IT, NL, PT. This chart uses information on securitised mortgage loans alone (potentially resulting in selection bias) and may not therefore be an accurate reflection of national mortgage markets. The latest observation for household debt to income is for quarter 1, 2022, for BE, DE, IE, ES, FR, IT, NL, AT, PT, SI and FI; quarter 4, 2021, for MT; quarter 3, 2021, for GR; quarter 4, 2020, for CY, EE, LT, LU, LV, SK.

It is important to distinguish between RRE and CRE markets given that they have different characteristics. For example, these two markets differ in terms of the types of actors, purposes of property purchases, and forms of financing.[5] RRE markets are mostly made up of domestic households purchasing properties for their own use or for buy-to-let purposes, and domestic banks that provide them with mortgage loans to finance those purchases. The perimeter of the market is limited to residential assets. In contrast, CRE markets are generally quite complex. First, CRE encompasses a wide range of real estate assets that are owned by firms for the purpose of generating income, such as office, retail, industrial and logistics properties but also multiple occupancy residential properties purchased by players other than households. Second, in addition to specialised CRE companies, the market players include banks, insurance companies and investment funds which invest in real estate to generate income by renting them out to other firms and households. Finally, international buyers also play a prominent role in CRE markets.

Different market structures in turn create different sources of financial stability risk and pose different challenges for financial stability analysis. While bank exposures to CRE markets are smaller than to RRE markets, CRE boom-bust cycles may still have serious implications for financial stability. However, the market’s complexity and the prevalence of data gaps pose special challenges for the CRE risk assessment and potential risk mitigation through macroprudential policy. These issues are therefore discussed in more detail in article 3. Given that the euro area banking system’s exposure to RRE markets is much greater than its exposure to CRE markets, and because the risk analysis and macroprudential tools for RRE are far more developed, the remainder of this lead article and articles 1 and 2 will focus on RRE risk and policy analysis in more detail.

A multi-dimensional approach, relying on several risk indicators and models, is required to assess financial stability risks from RRE markets. Since the GFC, the ECB, in conjunction with the national authorities, has developed a comprehensive framework for identifying the build-up of real estate vulnerabilities that could threaten financial stability.[6] Indicators for monitoring excessive price developments and overvaluation in property markets are important because they warn of imbalances that could lead to abrupt price corrections.[7] Furthermore, evidence suggests that the build-up of leverage is also a distinctive feature of housing booms that are dangerous for financial stability. Consequently, indicators for monitoring household debt and bank lending, including lending standards,[8] are required to identify unwarranted leverage and risk taking. At the same time, assessing household resilience sheds light on the credit risk of bank loan portfolios and on the potential for harmful declines in household expenditure should income or house prices drop. Finally, other imbalances that are often associated with real estate bubbles, including unsustainable developments in the construction sector, should also be monitored given that they often correlate with the costs of housing busts. Article 1 explains in more detail the methods and challenges for risk analysis of RRE markets. Ultimately, if financial stability risks from RRE markets are identified, macroprudential policy should use the appropriate tools to ensure the resilience of banks to any risk materialisation and/or to mitigate vulnerabilities.

2 Macroprudential policy tools to address RRE risks

In the wake of the GFC, macroprudential policy frameworks were set-up to mitigate financial stability risks.[9] The ultimate objective of macroprudential policy is to preserve financial stability to ensure the continuous and effective provision of key financial services to the real economy, even in periods of economic distress. To achieve this, macroprudential policy aims to identify early on any potential systemic risks that could endanger financial stability if they materialised. Macroprudential policy then applies appropriate tools to contain any further build-up of the risks identified (i.e. “leaning against the wind”) and to strengthen the financial system’s resilience to the potential materialisation of those risks. To mitigate financial stability risks from RRE markets, a large variety of tools are available that are enshrined in either European or national legislation.[10]

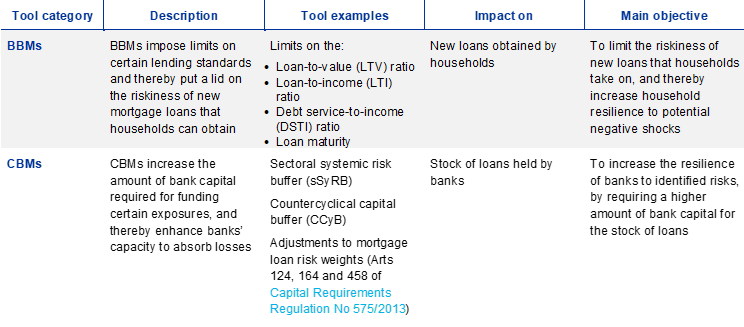

Macroprudential policy tools for real estate-related vulnerabilities include borrower-based measures (BBMs) and capital-based measures (CBMs). Borrower-based measures directly constrain new credit flows by imposing limits on the amount of credit that a specific borrower can obtain, typically in relation to the value of the underlying collateral or the borrower’s income (Table 1). While they do not have an immediate impact on banks’ capacity to absorb losses, they gradually reduce the magnitude of potential future bank losses by making households more resilient to income, interest-rate and house-price shocks. In contrast, capital-based measures enhance banks’ capacity to absorb losses (Table 1), although they are unlikely to have a material impact on borrower risk characteristics or the magnitude of expected future losses. The current macroprudential toolkit contains more policy tools for addressing vulnerabilities in the RRE sector (see below for further details of the tools available), while possible measures to address vulnerabilities in CRE markets are more limited (see article 3).

BBMs impose limits on certain lending standards and thereby put a lid on the riskiness of new mortgage loans that households can obtain. The most common BBMs are limits on the loan-to-value (LTV) ratio, the loan-to-income (LTI) ratio, the debt service-to-income (DSTI) ratio, and the maximum maturity of new household mortgage loans. The main objective of these measures is to limit the riskiness of new loans that households take on, and thereby increase household resilience to potential negative shocks. Over the medium term, BBMs also lead to more resilient banks, given that safer new lending flows translate into safer bank loan portfolios over time.[11] Details of the transmission channels for BBMs and how they can help to ensure financial stability are discussed in article 2. However, their beneficial impact on financial stability apart, BBMs may also have “undesirable” distributional effects given that they may limit access by younger or poorer households to mortgage loans.

Table 1

Macroprudential policy tools for RRE-related vulnerabilities include BBMs and CBMs

Source: ECB

CBMs increase the amount of bank capital required to fund certain exposures, and include various capital buffers and risk-weight measures. The key macroprudential capital tools in Europe for addressing financial stability risks from RRE markets are the countercyclical capital buffer (CCyB)[12], the sectoral systemic risk buffer (sSyRB) and adjustments to mortgage loan risk weights under Articles 124, 164 and 458 of the Capital Requirements Regulation (CRR)[13]. In contrast to BBMs, which only apply to newly originated loans, CBMs apply to the stock of outstanding bank loans. The main objective of CBMs is to increase the resilience of banks to identified risks, by requiring a higher amount of bank capital to be used for financing the relevant exposures. Should systemic risk materialise, the increased resilience makes it easier for banks to absorb losses while continuing to provide key financial services, thereby supporting economic activity and mitigating potential downward amplification effects through the financial system.[14] Details of the transmission channels for CBMs and how they can help to ensure financial stability are discussed in article 2.

In the banking union, responsibility for macroprudential policies to address real estate-related vulnerabilities is shared between the national authorities and the ECB.[15] Capital-based macroprudential tools for the banking sector are enshrined in European legislation (CRR/CRD framework), and the Single Supervisory Mechanism (SSM) Regulation provides the ECB with the power to tighten these tools beyond the levels set by national authorities in European banking supervision member countries if there is a need (“top-up” power). In contrast, borrower-based tools are governed by national legislation, they are not harmonised across the EU, and not all countries have a full set of borrower-based tools available.[16] The power to activate or adjust these instruments is in the exclusive remit of the national authorities. Finally, the ESRB may issue policy recommendations or warnings about real estate-related vulnerabilities in EU countries.[17]

3 Lessons from macroprudential policy implementation

In recent years, many European banking supervision member countries have activated multiple macroprudential policy tools to address RRE risks. In a context of booming RRE markets[18], the vast majority of European banking supervision member countries have activated combinations of different BBMs (see Table 2). These countries have generally opted for LTV limits combined with limits on the DSTI ratio and on the maximum maturity. Moreover, around half of European banking supervision countries have implemented risk-weight or capital buffer policies, at least in part, to respond to RRE vulnerabilities. In many cases, CBMs and BBMs were implemented jointly, suggesting that these macroprudential policy tools are primarily viewed by the national authorities as being complementary rather than as substitutes for each other (see article 2 for further details of the interaction between CBMs and BBMs).

A key lesson from the past years of macroprudential policy implementation is that the main objective has often been to increase resilience. When communicating the goal of macroprudential measures for real estate, authorities mainly emphasised the need to increase resilience to the potential future materialisation of systemic risk. Essentially, the main goal of authorities was to reduce the adverse feedback loops between the financial sector and the real economy that could emerge in periods of economic distress. While national authorities often justified the activation of macroprudential tools on the grounds of emerging imbalances and “excesses” in real estate markets, the objective of directly limiting the build-up of imbalances through macroprudential policy was often only of secondary importance. This was mainly due to the significant challenges of limiting the pace of accumulation of imbalances. These challenges related to the complex and uncertain transmission of macroprudential policy to credit and house prices and the lack of operational targets for these variables.

Table 2

In recent years, many European banking supervision member countries have activated multiple macroprudential policy tools to address RRE risks

Sources: ECB.

Note: measures in place as of 1 August 2022. CCyB rates are the ones announced by national authorities. FTB stands for first time buyer, SSB stands for second and subsequent buyer, BTL stands for buy to let, LGD stands for loss given default, IRB stands for internal ratings-based approach, STA stands for standardised approach banks.

The following countries have no measures in place and are therefore not included in the table: Spain, Greece and Italy.

Specific national measures are not always comparable given different definitions of loans, value/collateral and/or income.

The borrower-based measures in Austria, Belgium, Portugal and Slovenia (only the LTV limit in the case of the latter) are in the form of non-legally binding recommendations.

The sign (*) means that exceptions and/or further details apply. Please refer to national authorities’ websites.

BBMs have often been implemented in a structural manner as prudent back-stops, but with some embedded flexibility to limit undesired side effects. Due to the fact that BBMs only affect new lending flows and not existing loan stocks, it can take many years for their full effect to be felt in terms of borrower and bank resilience. Moreover, the activation or adjustment of BBMs often entails lengthy parliamentary and legal processes. Both factors may explain why many SSM member countries have implemented BBMs as “structural” (or “permanent”) measures in the nature of a back stop. This means that the limits imposed on lending standards are activated before clear excesses are visible and are not necessarily binding on implementation; they ensure, however, that there is a cap on potential future lending excesses. In addition, most countries have opted for caps differentiated by type of borrower and for exemption quotas permitting a proportion of new loans to exceed the limits imposed. This embedded flexibility into the design of BBMs may help to lower their social costs, while providing insurance against potential future lending excesses.

Experience to date suggests that CBMs unfold their full stabilisation potential if they are activated in a timely manner during upswings, so that they are available for release during crises. When activating capital-based macroprudential tools authorities usually aim to build banking system resilience commensurate to the systemic risks that are present at that time. However, the events of the past few years suggest that a premium can be put on timely activation of CBMs during upswings. First, there is always uncertainty about the true level of systemic risk within the system. Second, the economic costs of building up bank capital are generally low when the economy is expanding and banks are making profits (article 2).[19] Hence, timely activation of CBMs during upswings ensures that banking system resilience is there in case of need, without imposing a high cost on society. If systemic risk materialises and a crisis ensues, the release of capital measures that have been built up in good times is equally important: the release of CBMs increases capital headroom and eases regulatory pressure on banks, allowing them to absorb losses while continuing to provide key financial services.[20] This in turn may help to cushion an economic downturn and avoid additional losses in the banking sector.

BBMs and CBMs are mostly seen as policy tools that are complementary to each other and many countries have implemented them jointly. Although BBMs and CBMs both increase banking sector resilience and reduce macro volatility over the medium term (albeit through different transmission channels; see article 2 for further discussion of this matter), they are mostly seen as complementing each other, particularly over shorter time horizons. The reason for this complementarity is that BBMs mostly work on the flow of new mortgages, thus constraining any further build-up of vulnerabilities, but only gradually improve the risk characteristics of the mortgage loan stock. In contrast, CBMs apply directly to the existing mortgage stock and thereby enhance resilience against vulnerabilities that have accumulated in the past. As a result, many countries in the banking union have implemented BBMs and CBMs simultaneously (see the overview in Table 2). In summary, a comprehensive assessment of the interactions between these policy tools is necessary to tailor the policy mix to the specific situation in each country.

While considerable progress has been made, some challenges remain in relation to the calibration of instruments and measurement of their effectiveness. Given their importance for the macroeconomy and financial stability, RRE markets have been a focal point for macroprudential policy making in the banking union in recent years. Authorities in many countries have activated BBMs and CBMs that have helped to address vulnerabilities identified. However, assessing the effectiveness and the adequacy of these measures remains a continuous and challenging task for policy makers (see further discussion in article 2), given that constant monitoring and potential adjustment of instruments is necessary to ensure that the most appropriate policy mix is implemented at any one time. Moreover, the toolkit constantly evolves, and the addition of new instruments, such as the sSyRB, to the EU framework calls for further reflection on the proper calibration and the degree of interaction between new and existing (capital and borrower-based) instruments.

References

Behn, Markus, Rancoita, Elena, Rodriguez d’Acri, Costanza (2020), "Macroprudential capital buffers – objectives and usability", Macroprudential Bulletin, ECB, Frankfurt am Main.

Case, Karl E., Quigley, John M. and Shiller, Robert J. (2005), “Comparing Wealth Effects: The Stock Market versus the Housing Market”, Advances in Macroeconomics, Vol. 5, Issue 1, Article 1, pp. 1-34, May.

Cerutti, Eugenio ,Claessens, Stijn, and Laeven, Luc (2017), “The use and effectiveness of macroprudential policies: New evidence”, Journal of Financial Stability, Vol. 28, pp. 203-224.

Claessens, Stijn, Kose, M. Ayhan, and Terrones, Marco E. (2009), “What happens during recessions, crunches and busts?”, Economic Policy, Vol. 24, Issue 60, pp. 653–700.

Crowe, Christopher, Dell’Ariccia, Giovanni, Igan, Deniz, and Rabanal, Pau (2013), “How to deal with real estate booms: Lessons from country experiences”, Journal of Financial Stability, Vol. 9, Issue 3, pp. 300-319.

Constâncio, Vítor, Cabral, Inês, Detken, Carsten, Fell, John, Henry, Jérôme, Hiebert, Paul, Kapadia, Sujit, Altimari, Sergio Nicoletti, Pires, Fátima and Salleo, Carmelo (2019), “Macroprudential policy at the ECB: Institutional framework, strategy, analytical tools and policies”, Occasional Paper Series, No 227, ECB, Frankfurt am Main, July.

Di Casola, Paola, Dieckelmann, Daniel, Grothe, Magdalena, Hempell, Hannah, Jarmulska, Barbara, Lang, Jan Hannes and Rusnák, Marek (2021), “Bank capital buffers and lending in the euro area during the pandemic – Special Feature”, Financial Stability Review, ECB, Frankfurt am Main, November.

Di Casola, Paola, Dieckelmann, Daniel, Grothe, Magdalena, Hempell, Hannah, Jarmulska, Barbara, Lang, Jan Hannes and Rusnák, Marek (2022), “Drivers of rising house prices and the risk of reversal – Box 2”, Financial Stability Review, ECB, Frankfurt am Main, May.

Dierick, Frank, Point, Emmanuel, Cornacchia, Wanda and Pirovano, Mara (2017), “Closing real estate data gaps for financial stability monitoring and macroprudential policy in the EU”, Chapter in Data needs and statistics compilation for macroprudential analysis, vol. 46, Bank for International Settlements.

Duca, John V., Muellbauer, John, and Murphy, Anthony (2021), “What Drives House Price Cycles? International Experience and Policy Issues”, Journal of Economic Literature, Vol. 59, Issue 3, pp. 773-864.

European Central Bank (2016), Macroprudential Bulletin, Issue 1, Frankfurt am Main, March.

European Central Bank (2019), Financial Stability Review, Frankfurt am Main, November.

European Central Bank (2021), Financial Stability Review, Frankfurt am Main, November.

European Central Bank (2022), Financial Stability Review, Frankfurt am Main, May.

European Systemic Risk Board (2014), “Flagship Report on Macro-prudential Policy in the Banking Sector”, ESRB Instruments Working Group, Frankfurt am Main, March.

European Systemic Risk Board (2018), “The ESRB handbook on operationalising macroprudential policy in the banking sector”, ESRB Instruments Working Group, Frankfurt am Main, January.

European Systemic Risk Board (2019a), “Methodologies for the assessment of real estate vulnerabilities and macroprudential policies: residential real estate”, Working Group on Real Estate Methodologies, Frankfurt am Main, September.

European Systemic Risk Board (2019b), “Vulnerabilities in the residential real estate sectors of the EEA countries”, Frankfurt am Main, September.

European Systemic Risk Board (2022), “Vulnerabilities in the residential real estate sectors of the EEA countries”, Frankfurt am Main, February.

Gross, Marco and Población, Javier (2017), “Assessing the efficacy of borrower-based macroprudential policies using an integrated micro-macro model for European households”, Economic Modelling, Vol. 61, Issue Supplement, December, pp. 510-528.

Jordà, Òscar, Schularick, Moritz and Taylor, Alan M. (2015), “Leveraged bubbles”, Journal of Monetary Economics, Vol. 76, Issue Supplement, December, pp. S1-S20.

Jurča, Pavol, Klacso, Ján, Tereanu, Eugen, Forletta, Marco, Gross, Marco (2020), “The effectiveness of borrower-based macroprudential measures: a quantitative analysis for Slovakia”, IMF Working Paper, No. 20/134.

Lang, Jan Hannes, Pirovano, Mara, Rusnák, Marek and Schwarz, Claudia (2020), “Trends in residential real estate lending standards and implications for financial stability”, Financial Stability Review, ECB, Frankfurt am Main, May.

Lo Duca, Marco, Koban, Anne, Basten, Marisa, Bengtsson, Elias, Klaus, Benjamin, Kusmierczyk, Piotr, Lang, Jan Hannes, Detken, Carsten and Peltonen, Tuomas (2017), “A new database for financial crises in European countries: ECB/ESRB EU crises database”, Occasional Paper Series, No 194, ECB, Frankfurt am Main, July.

Lo Duca, Marco, Pirovano, Mara, Rusnák, Marek and Tereanu, Eugen (2019), “Macroprudential analysis of residential real estate markets”, Macroprudential Bulletin, ECB, Frankfurt am Main.

Lo Duca, Marco, Lang, Jan Hannes, Jarmulska, Barbara, Rusnák, Marek and Bandoni, Emil (2021), “Assessing the strength of the recent residential real estate expansion – Box 2”, Financial Stability Review, ECB, Frankfurt am Main, November.

Müller, Karsten & Verner, Emil (2021), “Credit Allocation and Macroeconomic Fluctuations”, SSRN Electronic Journal.

For topical analyses of RRE markets, see also Box 2 in the November 2021 issue of the Financial Stability Review and Box 2 in May 2022 issue of the Financial Stability Review. Country-level assessments of RRE vulnerabilities, which also draw on ECB input, were published by the European Systemic Risk Board (ESRB) in 2019 and 2022 (see ESRB, 2019b, and ESRB, 2022).

See Jordà, O. et al. (2015), Claessens, S. et al. (2009), Crowe, C. et al. (2013), Müller, K. and Verner, E. (2021) and Cerutti, E. et al. (2015).

See also Case, K.et al. (2005).

See Lo Duca, M. et al. (2019) and ESRB (2019a).

There are many lending standards data gaps within Europe. The ESRB therefore issued recommendations in 2016 and 2019 to national authorities aimed at closing these data gaps; see Recommendation of the European Systemic Risk Board of 31 October 2016 on closing real estate data gaps (ESRB/2016/14) (OJ C 31, 31.1.2017, p. 1) and Recommendation of the European Systemic Risk Board of 21 March 2019 amending Recommendation ESRB/2016/14 on closing real estate data gaps (ESRB/2019/3) (OJ C 271, 13.8.2019, p. 1). A financial stability assessment of developments in RRE lending standards in the euro area, based on a dedicated one-off data collection exercise by ECB Banking Supervision, can be found in Lang, J.H. et al. (2020).

See, for example, ESRB (2014) or ECB (2016).

See ESRB (2018) for a comprehensive overview.

See Gross, M. and Población, J. (2021) and Jurča, P. et al. (2020).

The CCyB is the main tool to be used for systemic risks related to excessive credit growth and leverage. As credit-fuelled RRE booms are often at the heart of wider credit booms, the CCyB is often activated in response to developments in RRE markets.

See Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012 (OJ L 176, 27.6.2013, p. 1).

For details see Box 8 entitled “Transmission and effectiveness of capital-based macroprudential policies” in the May 2022 issue of the ECB Financial Stability Review.

See, for example, ECB (2016), Constâncio, V. et al. (2019) or ECB (2019).

Even if the legislative framework for certain BBMs is not available, soft forms of BBMs can still be implemented through supervisory guidance on lending standards. This has been applied for example to Austria, Belgium, Portugal, and Slovenia.

For the most recent set of warnings and recommendations, see ESRB (2022a).

For an overview of systemic risks in RRE markets, see Section 1.5 of the May 2022 issue of the ECB Financial Stability Review, Box 2 entitled “Assessing the strength of the recent residential real estate expansion” in the November 2021 issue of the ECB Financial Stability Review and the February 2022 ESRB report entitled “Vulnerabilities in the residential real estate sectors of the EEA countries”.

See Box 8 entitled “Transmission and effectiveness of capital-based macroprudential policies” in the May 2022 issue of the ECB Financial Stability Review.

See Behn, M. et al. (2020) and Special Feature entitled “Transmission and effectiveness of capital-based macroprudential policies” in the November 2021 issue of the ECB Financial Stability Review.